Sometimes people are confused about the differences between FHA and conventional loans. In some cases, an FHA loan can help you buy a home sooner than you’d be able to buy with a conventional loan. Paperwork and processing times for both loan types are roughly the same, so it just comes down to what you qualify for and what makes the most financial sense for you. Let’s break down both loans.

What is a Conventional Loan?

A conventional home loan is a loan that isn’t guaranteed by any government agency like the VA, FHA, or USDA. However, these loans still have to conform to certain guidelines.

What is an FHA Loan?

An FHA (or Federal Housing Administration) loan is guaranteed by the government. Because it’s guaranteed, it’s less risky for lenders, and they can lower their qualification requirements.

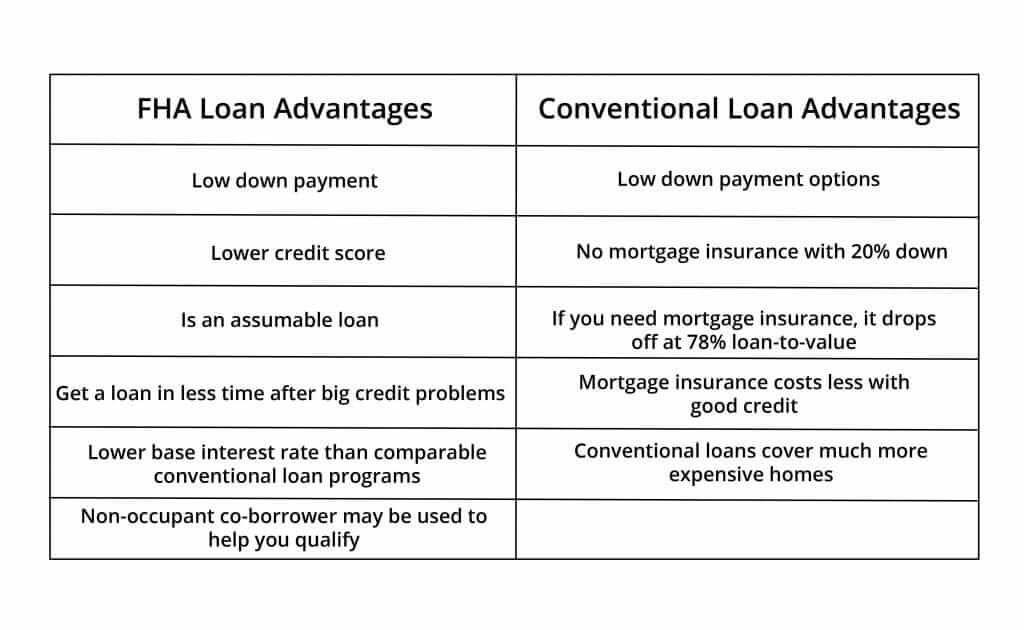

FHA loans are ideal for borrowers with lower credit (below the standard 620 cutoff for a conventional loan) or who don’t have much money available for a down payment (especially if some of their down payment money is being gifted to them). In some cases, an FHA loan may be the only way someone can buy a home.

Eligibility

Conventional

Credit score: Go here for information about conventional loan credit requirements.

Down payment: At least 20% to avoid mortgage insurance, but you can get a conventional loan with as little as 3% down.

Bankruptcy/foreclosure: You’ll need to wait seven years after a foreclosure and four years after a bankruptcy to be eligible.

FHA

Credit score: Go here for information about FHA loan credit requirements.

Down payment: Only those with scores of 580 and above qualify for putting 3.5% down. Those with lower scores must put at least 10% down.

Bankruptcy/foreclosure: Need to wait three years after a foreclosure and two years after a bankruptcy to be eligible.

Qualifying income: With an FHA loan, you can also use the income of a non-occupant co-borrower to qualify for the loan. Their income and debt will be blended with yours.

Mortgage Insurance

Conventional

With a conventional loan, you pay monthly private mortgage insurance (PMI) if you put less than 20% down on the home. The amount you pay is risk based, which means that those with high credit scores pay less, and those who put a higher percentage down pay less (if you put 10% down, you’ll pay less than if you put 5% down).

Even if you do need mortgage insurance, it drops off once the loan is down to 78% of the value of the home.

FHA

With an FHA loan, you’ll pay an upfront mortgage insurance premium at closing. The amount is 1.75% and is typically bundled with the loan amount. You’ll also pay an annual premium for the life of the loan, and that amount varies depending on several factors, but it’s around .50 to 1%. You can’t get rid of this cost unless you refinance to a different loan program.

Closing Costs

Conventional

Conventional loans have some restrictions on the origins of your down payment money. You may not be able to get a loan if all of your down payment is a gift from a relative.

FHA

FHA loans let borrowers use money from a non-profit, government agency, or relative to pay 100% of their down payment.

FHA Limitations

FHA loans can’t be used on investment properties or second homes. They’re also limited to the loan amount for your area. The amount in most places is $453,100.

Still not sure what kind of loan is best for you? Or are you ready to get started on an application? I’m here to help you make the decision that’s best for you and your finances, so please reach out!

No comments found.